Rental property calculator: what numbers actually matter?

I've watched a lot of people analyze deals on calculators and walk away with a number they trusted. The number was usually wrong, and not because the calculator was broken. They just didn't include the whole picture. The calculator dutifully gave them a profitable-looking garbage number back, so they bought the property. Reality showed up about six months later with a roof estimate.

So the framing I'd push instead: a calculator isn't there to confirm your deal works. It's there to tell you whether it still works when reality hits. Here are the seven inputs you need to actually decide that, plus one bonus.

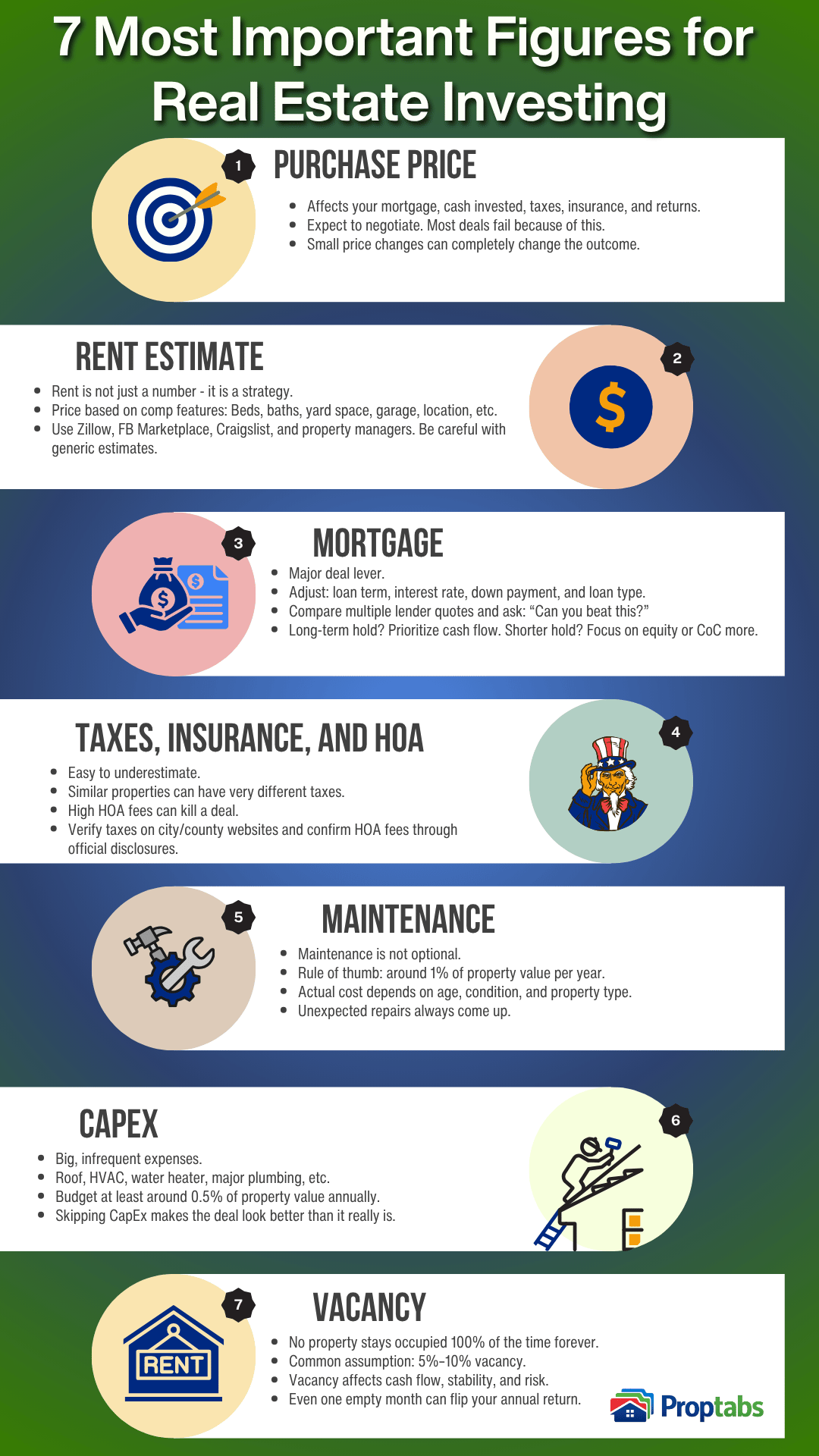

1. Purchase price

This drives everything else including the mortgage payment, potential taxes, insurance premiums, cash invested, and return on investment. I run three versions for every deal: asking price, my offer price, and the "deal price" where the numbers actually sound good. The gap between those three is often where you find out whether you should walk.

2. Rent estimate

Most people treat rent as a fixed input. They pull comps, plug in the average, and move on. Rent is a strategy, not a constant, and this is where I see the biggest gap between sloppy analysis and good analysis.

When I house hacked my place, I started with a guess of about $300 per room. Then I actually looked at what 1-bedroom apartments nearby were going for, which was $800 to $1,200 at the time, and I noticed my property had things those apartments didn't: a yard, shared living spaces, and better amenities overall. So I broke it down further. Bigger rooms were priced higher. Private bathroom became a premium. Walk-in closet plus vanity, another premium. I even rented a garage spot out for an extra $50/mo. The whole thing came in around $2,200/mo total, which was wildly off from my original mental math. I also lived there rent free, and made some long-lasting friendships along the way.

Tool-wise, I tend to focus on actual similar listings. I'll check Zillow rentals, Craigslist, and Facebook Marketplace. Zillow's Rent Zestimate is fine for vanilla single-family rentals but it's not even close on room-by-room or house hack setups. I've seen it underestimate by 40% or more on those.

3. Mortgage

Treating the mortgage as fixed is the second biggest mistake after rent. Loan term, rate, down payment, and loan type are all things you can adjust, and what you optimize for depends on what you're actually doing with the property. If you're holding long-term, you need cash flow, so prioritize a longer term and a lower monthly payment. Selling in a few years, a shorter term helps build equity faster, which can cover selling costs.

Get quotes from multiple lenders and play them off each other. Forward the best one to the others and ask if they can beat it. They often can. If this feels rude the first time you do it, it's not. It's the entire structure of the industry, and they expect it.

Example: $300,000 purchase price

| Scenario | Rate | Term | Down | Monthly P&I |

|---|---|---|---|---|

| Long-term hold | 7.0% | 30yr | 20% ($60k) | $1,597 |

| Shop lenders (rate negotiated down) | 6.5% | 30yr | 20% ($60k) | $1,517 (-$80/mo) |

| Build equity faster | 7.0% | 15yr | 20% ($60k) | $2,157 (+$560/mo) |

| Put more down | 7.0% | 30yr | 25% ($75k) | $1,498 (-$99/mo) |

Negotiating 0.5% off your rate saves $960/year. That same money funds most of your CapEx reserve.

4. Taxes and insurance

These vary in ways that look random. I own a few duplexes in the same zip code with similar features, and one of them has almost 3x the property tax of the others. I don't have a great explanation. Assessments are uneven and sometimes the answer is just "yeah, that's what it is." You can sometimes appeal taxes to get a lower payment, but don't count on it when making purchasing decisions.

The one I'll never forget was a place I almost bought that seemed like a steal on the listing, until I dug into the HOA and found a $600/month fee buried in the disclosure. That single line item killed it. Don't trust listing data for taxes or HOA. Pull the county tax records and the actual HOA disclosure docs, every time.

5. Maintenance

The standard rule is 1% of property value, annually. Some years you'll be under it, and some years a leaking water line will eat your whole budget in March. Whatever you assume, it won't be zero, and on my first deal I underestimated it badly. The renovation work I budgeted for at purchase was the easy part, but what blindsided me was that the maintenance just kept going. There's no version where the property is "done", especially with tenants.

6. Capital Expenditures

Big, infrequent costs like the roof, HVAC, or water heater. I had to replace a roof out-of-pocket for $11,000, which on a property doing a few hundred a month in cash flow wipes out several years of profit in one check. Budget at least 0.5% of property value annually for this and treat that money as already spent. If your calculator doesn't have a CapEx line, it's lying to you, no cap.

A tornado came through and ripped the siding clean off this property. You can never really know and plan for everything. In this case, insurance helped out, but it's a good reminder that the unexpected will happen.

7. Vacancy

Nothing rents 100% of the time forever. Plan for 5 to 10%. The thing people miss is that vacancy isn't just a cash flow hit, it's also where your risk lives. A property that only cash flows when it's fully occupied isn't really cash flowing. It's gambling with the lights on.

Bonus: Property management

I know, you're going to self-manage. Most people do at first. The question is whether your analysis still works when you stop, and you will stop eventually, especially if you scale. Standard cost is around 10% of rent, plus a portion of a month's rent after signing a new tenant. Run the numbers with management included even if you're managing yourself today, and if the deal collapses under that line, you don't have a deal. You have a job.

Quick reference: typical expense ranges

Use these as a starting point. Every market is different, and you should verify each number for your specific property.

| Expense | Typical rate | What to watch for |

|---|---|---|

| Taxes | 0.5%–2.5% of value/yr | Pull county records, not listing data |

| Insurance | 0.3%–0.5% of value/yr | Higher in flood or wind-prone areas |

| Maintenance | ~1% of value/yr | Budget more for older properties |

| CapEx | ~0.5% of value/yr | Roof, HVAC, water heater. Treat it as already spent. |

| Vacancy | 5%–10% of annual rent | Keep 1 to 2 months of rent in reserve |

| Management | ~10% of monthly rent | Include even if you are self-managing today |

The fantasy vs. the math

| Line item | Simple math | Real numbers |

|---|---|---|

| Rent | $2,500 | $2,500 |

| Mortgage | $2,100 | $2,100 |

| Taxes | not counted | $300 |

| Insurance | not counted | $125 |

| Maintenance | not counted | $200 |

| CapEx | not counted | $100 |

| Vacancy | not counted | $125 |

| Management | not counted | $250 |

| Total expenses | $2,100 | $3,200 |

| Monthly cash flow | +$400 | -$700 |

A property that the spreadsheet said was netting you $400 is actually bleeding $700. I've seen variations of this exact arithmetic destroy people's first deals.

Why I stopped using Excel

I used spreadsheets for years and they were fine, mostly. The problems weren't dramatic, just persistent. Formulas broke when I duplicated templates, sharing with a partner or a lender was clunky, and the model didn't flex well for house hacks and short-term rentals. So I built PropTabs around the principle that you can't skip the unfun lines. Maintenance, CapEx, vacancy, and management are all included in the calculator. You don't get a real result unless you've put real numbers in. If a deal looks great in PropTabs, I feel confident moving forward.

The thing nobody tells beginners

Beginners ask whether the deal works. People who've been doing this for a while ask what would have to be wrong for it to fail. And then they go check whether any of those things might actually be wrong. That's the move. Many deals look fine on a quick analysis. The honest version of the analysis is what separates the deals you should make an offer on from the ones you should walk away from, which is arguably the greatest strength of a successful investor.

If you're staring at a potential deal right now, run it through PropTabs and see what comes out. It might make financial sense, or it might scare you away, but either way it's a win.

About the author

Jonah Jamesen

Jonah Jamesen is a real estate investor who converted a foreclosed 5-bedroom home into a fully renovated house hack generating $2,200/month while living there rent-free. He has hands-on experience with full gut renovations, room-by-room rentals, self-managing properties, and working with property management companies, all while holding down a full-time job. PropTabs is the deal analysis tool he built because he was tired of rebuilding the same spreadsheet for every property.